Day: June 15, 2017

-

Attracting Millennials into the Housing Ecosystem

Millennials have this enigmatic aura around them. Older generations scratch their heads trying to make sense of them as if they are extraterrestrials with green-and-white colored coffee cups in one hand and smartphones in the other, who bond by laughing together over memes on Instagram. Millennials comprise individuals between 18 to 34 years old, and,…

-

How to Get Your Economic Groove On, Part 2

While the Internet offers a plethora of primary data sources that can be tapped to gain a better understanding of economics and the housing market, along with them come even more sites offering interpretations of those primary data sources. While some of these sites may seem to serve an educational purpose, and in fact be…

-

Leadership Lessons on Women in the Real Estate Businesses

Women influence much of the business world today, and this is increasingly true when it comes to the business of real estate. In fact, the 2016 NAR Member Profile reveals that 62 percent of all REALTORS® are women. In my role as president of Leading Real Estate Companies of the World®, I have had the…

-

NWBC Entrepreneurial Ecosystems & Their Service of Women Entrepreneurs

Women entrepreneurs are on the rise, and they are leaving their footprint on the nation’s economy. In 2012, the U.S. Census Bureau reported an estimated 9.9 million women-owned firms, 35.8 percent of all U.S. firms classifiable by gender, and the total estimated receipts from those firms was $1.4 trillion. Nevertheless, women-owned businesses are still an…

-

Is the Mortgage Industry Painting with too Broad a Brush?

Becoming a homeowner helps safeguard a person’s professional achievements and can pull them out of poverty. However, current mortgage lending trends show that a significant portion of Americans are being all but excluded from homeownership by stringent credit-assessing practices leading to mortgage rejections. The Great Recession, which saw nearly 8 million American homes fall into…

-

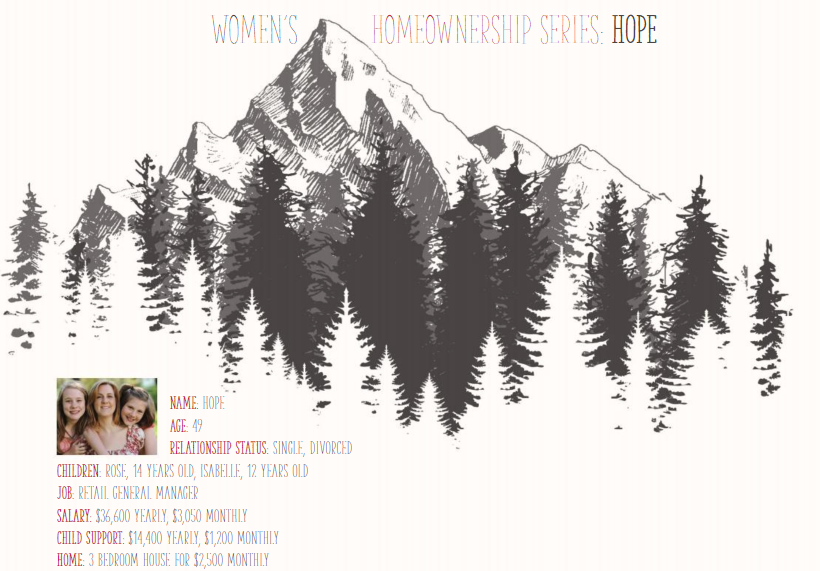

Women’s Homeownership Series: Hope

Hope and her husband, with their two daughters, moved into a beautiful 3 bedroom, 2 bathroom home in Boulder, Colorado two-and-a-half years ago. Previously living in a smaller 2 bedroom condominium a few miles away, the family enjoyed the comfort and convenience of a larger space. Their daughters, Rose and Isabelle, were happy to have…

-

The Changing Landscape of Single-Family Rental Homes

The Single-Family Rental (SFR) industry is growing fast, attracting families, millennials and baby boomers alike, who are drawn to the flexibility of renting. Our residents are America’s teachers, police officers and military families looking to rent homes in good neighborhoods with good schools. According to the U.S. Census Bureau’s American Community Survey (ACS), the percentage…

-

Vicky Silvano AREAA 2016 National Chairwoman

1. What is the experience of being the chairwoman of an organization like the Asian Real Estate Association of America (AREAA)? What was your favorite part of your work as chairwoman and your proudest achievement? Getting to the onset of being the leader of a big organization is overwhelming. Coming from the most quintessential immigrant…

-

The Future of Small Businesses

With limited employees, capital and resources, small businesses are hit the hardest by rigorous regulations, and the expense of compliance often poses sustainable growth roadblocks for the entrepreneurs who need it the most. The following months could prove especially pivotal for small business owners, as the possibility of new legislation and regulations grows. Access to…

-

The Movers & the Shakedown

America has long been crowned as the land of dreamers, the land of opportunity, and if you work hard enough and remain diligent, there is nothing you can’t achieve. The wealth is in land and labor, and it’s that which accumulates, you can control, and pass on to the next generation. Black people are not…