Tag: Hope

-

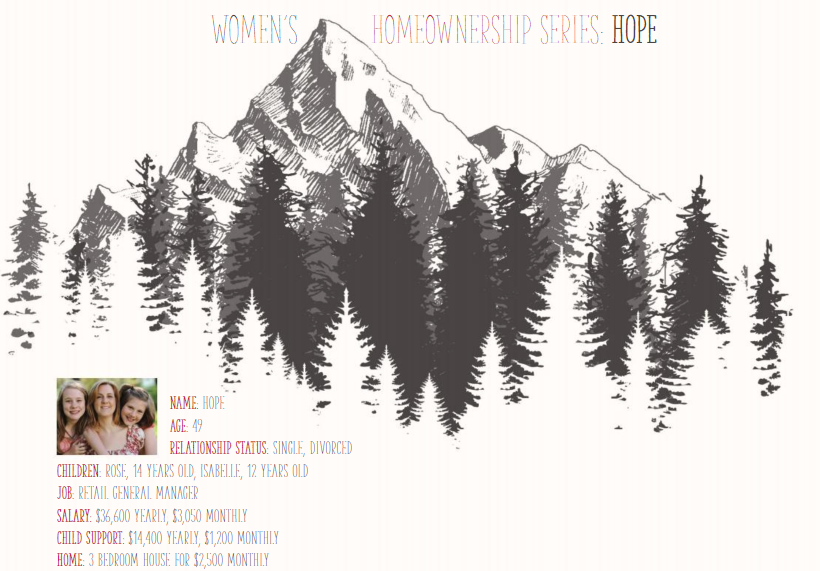

Women’s Homeownership Series: Hope

Hope and her husband, with their two daughters, moved into a beautiful 3 bedroom, 2 bathroom home in Boulder, Colorado two-and-a-half years ago. Previously living in a smaller 2 bedroom condominium a few miles away, the family enjoyed the comfort and convenience of a larger space. Their daughters, Rose and Isabelle, were happy to have…