Month: April 2015

-

The Reverse Mortgage that Will Save Seniors Money

Starting May 1, there will be a new way for seniors to attain reverse mortgages from what is called a Caregiver Loan. This loan will allow adult children or grandchildren of seniors to pool resources to provide a flexible line of credit at interest rates much lower than commercial reverse-mortgage lenders charge.

-

$140 Million Settlement Has Ocwen & Assurant Pay Up

Riddled with countless financial setbacks, Ocwen was dealt another heavy blow with a $140 million class action settlement that must be paid by both Ocwen and Assurant Inc. to homeowners who were given inflated premiums for force-placed insurance.

-

Serious Delinquency Rates on Single-Family Loans at an All-Time Low

The serious delinquency rate on single-family loans has fallen to its lowest level in six and a half years. Serious delinquency is when a single-family mortgage is 90 or more days past due and the bank considers the mortgage to be in danger of default. When a mortgage is in default, a lender usually initiates…

-

Update: Learn the Latest Developments at NAWRB

NAWRB is rapidly growing in presence and membership each day. Our corporate headquarters is buzzing with new business and exciting developments. With that being said, we’d like to share our growth with our readers to not only spread the enthusiasm but show what NAWRB is doing to advocate and promote for women in the housing…

-

The Mystery Behind Lending to Women

In her first appearance before the U.S. House of Representatives, the Administrator of the Small Business Administration (SBA), Maria Contreras-Sweet, recently said, “There is no silver bullet when it comes to access to capital.” This comes from a woman who left the California-based bank she founded to become Administrator. Her sentiments were brought into clear…

-

Professional Mentors: Why Women Need Them

Women can benefit a great deal by having professional mentors. Men already have an edge over females when it comes to earning appropriate wages and advancing to upper level management. Having smart, successful mentors for professional ladies can work wonders in bridging the inequality gap.

-

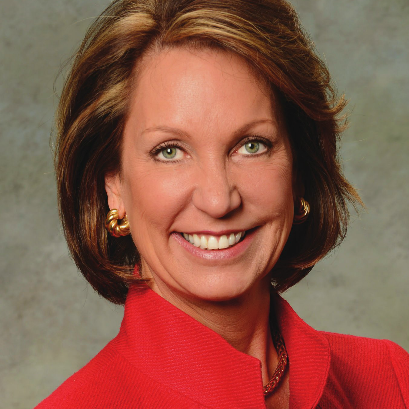

Margaret Kelly

RE/MAX’s CEO Powerhouse Margaret Kelly NAWRB is honored to have had the opportunity to have an insightful and candid interview with Margaret Kelly, CEO of RE/MAX. Kelly is responsible for the day-to-day operations and strategic direction at RE/MAX across North America and in more than 95 countries around the world. She is recognized by countless…

-

Best Strategies and Courses for Selling to Senior Buyers

The population of seniors in the United States is increasing rapidly due to the aging baby boomer generation. Some cities are experiencing rapid growth more so than others. It’s important for real estate agents to be aware of these locales and understand the best strategies for appealing to this growing demographic.

-

5 Key Traits of Successful Female Professionals

You may be a professional woman in the housing industry who is also a wife and mother. While you make your career a priority, you get busy. If you compare yourself to others, professionally and personally, know that it is an energy drainer and it can do a lot to negatively affect your mental health.…

-

Coming To A City Near You: Micro-Apartments

With the scarcity of affordable housing in metropolitan areas, are micro-apartments the future of housing? The tiny home movement and creation of micro-apartments has taken international cities by storm. The rise in micro-living can be attributed to a lack of available land for housing, surges in population, and booming economies in urban areas. Cities such…