Tag: homeowner

-

Boulder, CO: Best Housing Market for Growth & Stability

Homebuyers should think about buying their first home in Boulder, CO, as it is ranked the best housing market for growth and stability by a recent Smart Asset report. According to their findings, the odds of a major drop in home prices are 0 percent in the city, while properties have increased 268 percent in…

-

How Agents Can Better Serve Single-Women Homebuyers

Married couples might comprise the greatest share of homebuyers, but single women follow close behind, especially retired women over the age of 55, according to the Wall Street Journal. Gone are the days when women had to wait until marriage to buy a home; now, women are feeling more confident in creating their own sanctuary…

-

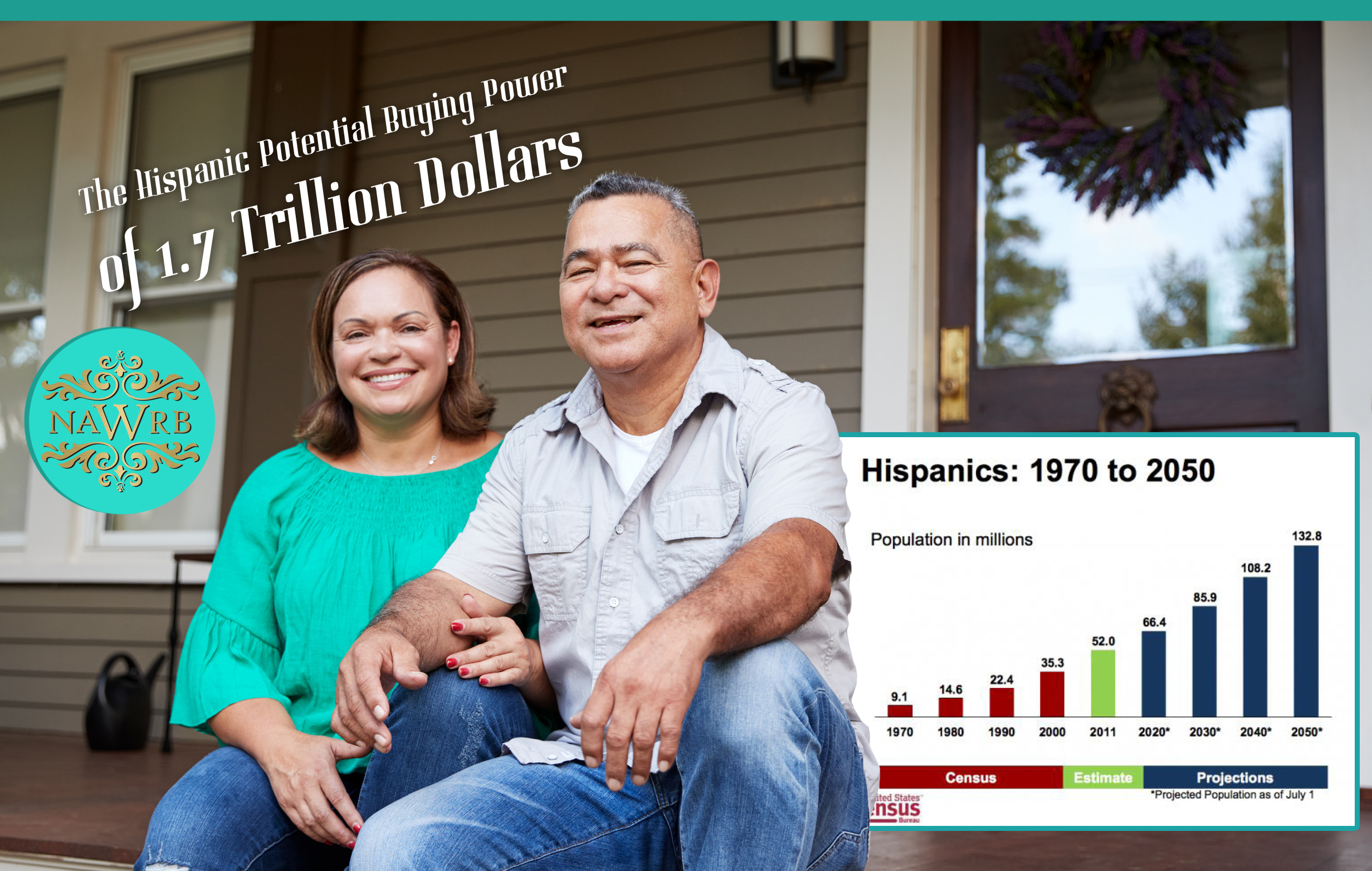

The Hispanic Potential Buying Power of 1.7 Trillion Dollars

The goal of every business is to make a profit and the real estate industry is no different. An often undermined market is the Hispanic and this article will help you uncover the potential within the Hispanic market that most overlook, which means millions of dollars for businesses looking to invest in this market. Tap…

-

Deadliest Fires in California 2018: Resources for Financial Recovery

After dealing with numerous deadly fires earlier this year, California is currently dealing with three major wildfires, including the Camp Fire in Butte County, the Woosley Fire in Los Angeles County and the Hill Fire in Ventura County. California Governor-elect Gavin Newsom recently issued emergency proclamations in response to the wildfires and requested statewide FEMA…

-

Attention All The Single Ladies: 5 Ways To Help You Become a Homeowner

Despite the pay gap, women are increasingly becoming financial powerhouses. Case in point: they now control 51 percent of American wealth, totaling some $14 trillion in assets. One of the ways they’re using those assets to their advantage? Home buying. According to the latest data from Ellie Mae, women are the primary borrowers on 32…

-

Agents: Closing Gifts for a Lasting Impression

The process of buying a home can be stressful for many buyers, especially first time home buyers. Luckily, real estate agents have the expertise to help clients navigate the process to find their perfect home. The constant interaction between buyers and agents can also result in the formation of strong bonds. What better way to…